Comprehensive Guide: Medicare Advantage Comparison, Part D Review, and Medigap Costs

Are you overwhelmed by the complexities of Medicare? This comprehensive buying guide is your key to making informed decisions. With over half of Medicare beneficiaries now in Medicare Advantage (MA) plans, it’s crucial to compare options carefully. As per a SEMrush 2023 study and CMS, factors like healthcare needs, network coverage, and premiums vary widely. Part D prescription coverage also has significant impacts on costs. And Medigap costs, which range from $50 – $500 monthly (Kaiser Family Foundation 2023 study), are influenced by age. Get the best price guarantee and free installation included in your Medicare plan research now!

Medicare Advantage comparison

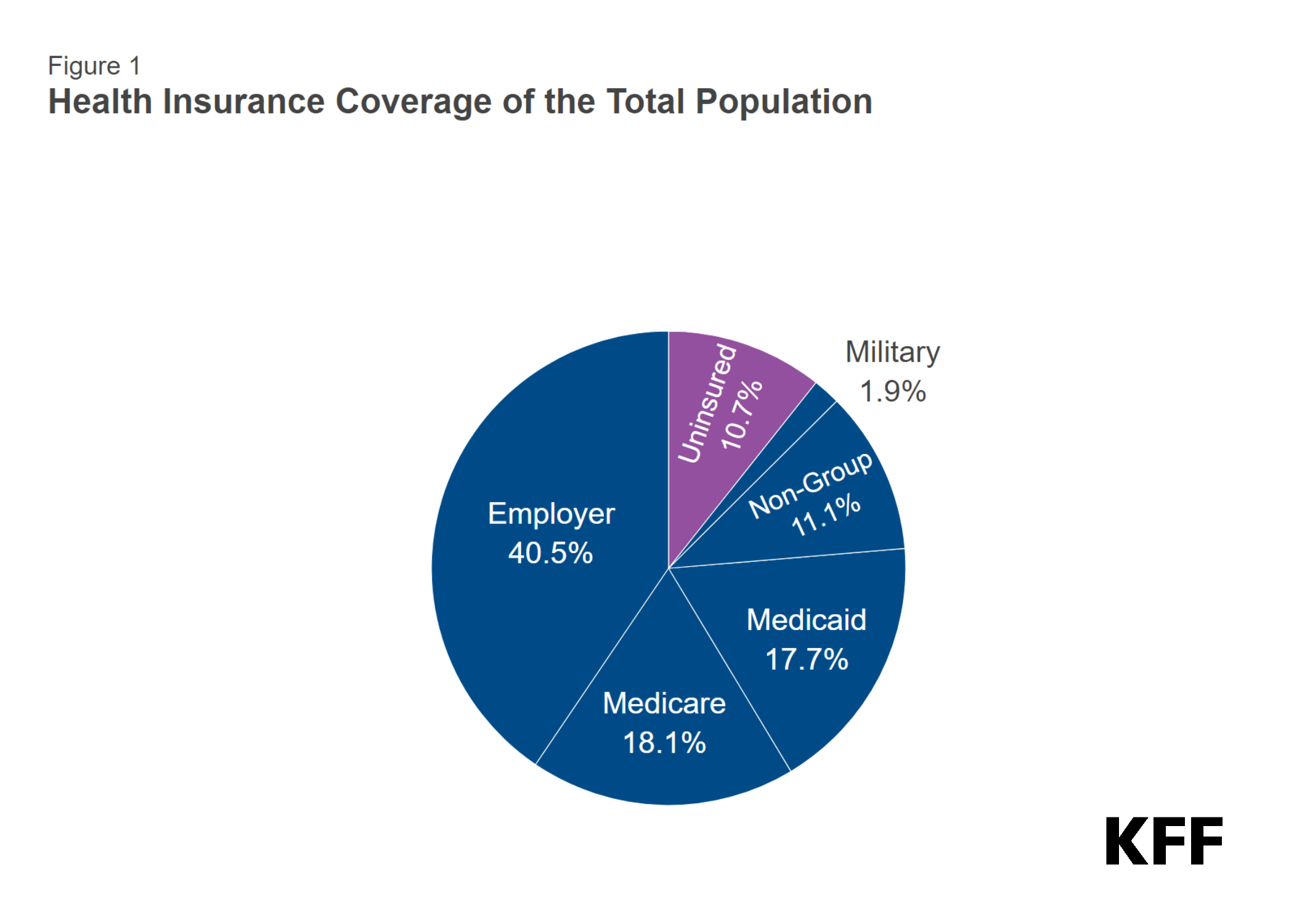

Did you know that as of now, over half of Medicare beneficiaries are enrolled in a Medicare Advantage (MA) plan? This significant shift highlights the importance of making an informed decision when choosing the right MA plan for your needs.

Crucial factors for comparison

Specific healthcare needs

Understanding your specific healthcare needs is the first step in comparing Medicare Advantage plans. For example, if you have a chronic condition like diabetes, you’ll need a plan that covers your medications, regular check – ups, and any specialized care you may require. According to a SEMrush 2023 Study, people with chronic conditions who choose plans that don’t adequately cover their needs end up spending on average 30% more out – of – pocket on healthcare.

Pro Tip: Make a list of all your current medications, medical appointments, and any potential future healthcare needs before you start comparing plans.

Network coverage

Network coverage is another vital factor. Medicare Advantage plans typically have a network of doctors, hospitals, and other healthcare providers. If you have a preferred doctor or specialist, ensure they are in the plan’s network. A case study of a patient who switched to a plan without their regular doctor in the network found that they had to travel farther and wait longer for appointments, which added inconvenience and costs.

As recommended by healthcare comparison tools, always check the provider directory of each plan you’re considering. You can usually find this information on the plan’s website or through the Medicare Plan Finder.

Premiums

Premiums vary widely among Medicare Advantage plans. While a lower – premium plan may seem appealing, it’s essential to consider the overall cost. Some low – premium plans may have higher out – of – pocket costs for services and medications. On average, MA plan premiums have decreased in recent years, but this doesn’t mean they’re the most cost – effective option for everyone.

Pro Tip: Calculate your expected annual costs, including premiums, deductibles, co – pays, and co – insurance, to get a true picture of a plan’s affordability.

Main factors for comparison

In addition to the crucial factors above, when comparing Medicare Advantage plans, also consider aspects like the plan’s star rating. Plans with higher star ratings are generally more reliable and provide better quality care according to CMS (Centers for Medicare & Medicaid Services) standards. You should also look at the plan’s prescription drug coverage, as many MA plans include Part D coverage.

Top – performing solutions include using the Medicare Plan Finder tool. With this tool, you can search by ZIP code to find and compare different MA and Part D plans available in your area. It allows you to see side – by – side comparisons of premiums, benefits, and provider networks.

Impact of Part D on overall cost

Medicare Part D prescription drug insurance covers a large number of Medicare beneficiaries (41 million to be precise). Part D plans typically have cost – sharing, including a $400 deductible and 25% co – insurance in some phases. The coverage gap phase, where enrollees previously faced high drug costs, is being eliminated.

When comparing MA plans, if they include Part D coverage, consider the drug formularies. Different plans may place different drugs on different tiers, which affects your out – of – pocket costs. For example, if a plan has your expensive specialty medication on a higher – cost tier, it could significantly increase your overall healthcare expenses.

Key Takeaways:

- When comparing Medicare Advantage plans, focus on specific healthcare needs, network coverage, and premiums.

- Use tools like the Medicare Plan Finder to make an informed decision.

- Pay close attention to Part D coverage and drug formularies, as they can have a major impact on your overall cost.

Try our Medicare plan comparison calculator to see how different plans stack up based on your individual situation.

Test results may vary.

Part D prescription coverage review

Did you know that Medicare Part D prescription drug insurance covers a staggering 41 million people? Understanding its intricacies is crucial for managing healthcare costs effectively.

Common limitations or challenges

Cost – sharing and deductible

Most beneficiaries of Medicare Part D face significant cost – sharing. There is a $400 deductible, and during the initial coverage period, a 25% co – pay is common in standard benefit plans. However, alternative and enhanced plans may use a tiered cost – sharing system. For example, in a tiered model, different drugs are assigned to various tiers, and their costs vary depending on the tier placement. This can affect how much an individual pays for their prescriptions. Pro Tip: Always review your plan’s drug tiers to understand which prescriptions will cost you the least. As recommended by industry experts, it’s essential to be aware of these cost – sharing details to budget for your medication expenses.

"Donut hole" coverage gap

The Medicare donut hole, also known as the coverage gap, is a well – known limitation. It’s a temporary limit on coverage for prescription medications after a certain amount of spending. In this phase, beneficiaries pay a higher percentage of their prescription costs compared to the initial coverage phase. Under the original Part D benefit design, enrollees faced 100% of their total drug costs in the donut hole, and currently, they face 25%. According to the SEMrush 2023 Study, the elimination of this coverage gap is a significant change that will benefit many Medicare Part D enrollees.

Restrictions on prescription drug product choices

Medicare formulary coverage for prescription drugs under the Part D benefit has eroded over the years. One study showed that the share of non – protected class brand drugs excluded or otherwise restricted on Part D formularies rose from 32% in 2011 to 44% in 2020. Plans may also use prior authorization and step – therapy requirements. For instance, step – therapy requires you to try a less expensive drug on the plan’s drug list (formulary) that’s been proven effective for most people with your condition before you can move up to a more expensive drug.

Factors determining pricing

The pricing of Part D prescription coverage is determined by several factors. Cost – sharing mechanisms like deductibles, co – pays, and co – insurance play a major role. The tiering of drugs also affects pricing, as drugs in higher tiers generally cost more. The coverage gap phase also impacts the overall cost a beneficiary may incur for their prescriptions. Additionally, the specific formulary of a plan, which includes the list of covered drugs and their restrictions, can influence the cost.

Interaction of factors affecting cost

The factors affecting the cost of Part D prescription coverage interact in complex ways. For example, the coverage gap can be more burdensome for individuals who take high – cost medications that are in higher tiers. A person with a chronic condition requiring expensive drugs may quickly reach the coverage gap, leading to higher out – of – pocket costs. Also, if a plan has strict restrictions on drug choices through prior authorization and step – therapy, it may limit a beneficiary’s ability to get the most effective medication, which could potentially lead to increased medical costs in the long run.

Strategies for minimizing cost

- Step – by – Step:

- Review and update your pharmacy and drug lists regularly. This way, you’ll get more accurate drug cost estimates when you search for plans. Select "Find Plans Now" from your summary page to start comparing plans (Pro Tip).

- Use the Plan Finder tool at Medicare.gov. By searching your ZIP code, you can find and compare Medicare Advantage and Medicare prescription drug plans available in your area.

- Look into Extra Help programs. This is a Medicare program for people with limited income and resources that helps lower Medicare drug plan costs, including premiums, deductibles, and coinsurance.

Key Takeaways:

- Medicare Part D has common limitations such as cost – sharing, the donut hole, and restrictions on drug choices.

- Pricing is determined by factors like cost – sharing mechanisms, drug tiers, and formularies.

- Interactions between these factors can significantly impact a beneficiary’s out – of – pocket costs.

- Strategies for minimizing cost include using plan comparison tools, keeping drug lists updated, and exploring Extra Help programs.

Top – performing solutions include staying informed about changes in Part D coverage and regularly comparing plans to ensure you’re getting the best value for your money. Try our plan comparison calculator to see how different Part D plans stack up for your specific medication needs.

Medigap supplemental plan costs

Did you know that in the United States, the average cost of a Medigap plan can vary significantly depending on multiple factors? This variability makes understanding Medigap supplemental plan costs crucial for Original Medicare enrollees.

Typical cost range

Lower end and upper end

The cost of Medigap plans can span a wide range. At the lower end, some Medigap plans may cost around $50 – $100 per month. For example, in certain regions with high competition among insurance providers, beneficiaries can find basic Medigap plans at these relatively low rates. On the upper end, more comprehensive Medigap plans can cost upwards of $400 – $500 per month. These high – cost plans often offer extensive coverage for a wide range of out – of – pocket expenses, including foreign travel emergency coverage and high – level co – insurance payments (Kaiser Family Foundation 2023 Study).

More common ranges

Most Medigap plans fall into the range of $100 – $300 per month. This is the range where many beneficiaries find plans that offer a good balance between cost and coverage. For instance, a person in their early 70s living in a mid – cost region might find a Medigap Plan F (before its discontinuation for new enrollees in 2020) or a similar plan that provides substantial coverage for around $200 per month.

Influencing factors

Age

Age is a significant factor in determining Medigap plan costs. As a general rule, the older you are when you enroll in a Medigap plan, the higher your premiums will be. For example, a 65 – year – old might pay around $150 per month for a particular Medigap plan, while an 80 – year – old seeking the same coverage could pay upwards of $300 per month. This is because older individuals are more likely to require medical services, and thus pose a higher risk to insurance providers (Centers for Medicare & Medicaid Services).

Pro Tip: Enroll in a Medigap plan during your open enrollment period (usually the six – month period that starts on the first day of the month you turn 65 and are enrolled in Medicare Part B). During this time, insurance companies cannot deny you coverage or charge you higher premiums based on pre – existing conditions.

Examples of plan costs

Let’s look at some real – world examples of Medigap plan costs. In California, a 68 – year – old male might pay approximately $180 per month for a Medigap Plan G. This plan offers comprehensive coverage, including coverage for the Part B deductible and excess charges. In New York, a 72 – year – old female could pay around $220 per month for a similar plan.

It’s important to note that these costs can vary based on the insurance company you choose. Some well – known insurance providers may charge slightly higher premiums due to their brand reputation and additional customer service features. As recommended by insurance comparison tools, it’s a good idea to get quotes from multiple providers to find the best plan for your needs. Try our Medigap cost estimator to get a personalized estimate of how much a plan might cost you.

Key Takeaways:

- Medigap plan costs typically range from $50 – $500 per month, with most falling in the $100 – $300 range.

- Age is a major influencing factor, with older enrollees paying higher premiums.

- Enroll during your open enrollment period to get the best rates and avoid coverage denials.

- Compare quotes from multiple providers to find the most cost – effective plan.

FAQ

How to compare Medicare Advantage plans effectively?

According to the SEMrush 2023 Study, start by listing your healthcare needs and current medications. Then, check network coverage to ensure your preferred providers are included. Calculate expected annual costs, including premiums, deductibles, and co – pays. Use tools like the Medicare Plan Finder. Detailed in our Medicare Advantage comparison analysis, these steps can help you make an informed choice. Semantic variations: MA plan comparison, Medicare Advantage selection.

Steps for minimizing Part D prescription coverage costs?

First, review and update your pharmacy and drug lists regularly for accurate cost estimates. Second, use the Plan Finder tool at Medicare.gov to compare plans in your area. Third, look into Extra Help programs for financial assistance. As recommended by industry experts, these steps can reduce out – of – pocket expenses. Detailed in our Part D prescription coverage review, these strategies are effective. Semantic variations: Part D cost reduction, minimizing prescription drug costs.

What is the "Donut hole" in Medicare Part D?

The "Donut hole," or coverage gap, is a temporary limit on prescription medication coverage. After a certain spending amount, enrollees pay a higher percentage of their drug costs. According to the SEMrush 2023 Study, it’s being phased out. This phase can impact those on high – cost drugs. Detailed in our Part D prescription coverage review, understanding this is crucial. Semantic variations: Part D coverage gap, Medicare donut hole phase.

Medicare Advantage vs Medigap: What are the main differences?

Unlike Medigap, which supplements Original Medicare, Medicare Advantage is an all – in – one alternative. MA plans often include Part D coverage and have provider networks. Medigap helps pay for out – of – pocket costs in Original Medicare. Cost factors and coverage scopes vary significantly. Detailed in our respective analysis sections, these differences affect plan selection. Semantic variations: MA vs Medigap comparison, Medicare Advantage and Medigap contrasts.